supermoney

Your money stress, solved by AI.

SuperMoney Has Been a Comparison Site for Years. Now It Wants to Be the Thing That Actually Tells You What to Do.

The Macro: The Gap Between Knowing and Doing

Most personal finance tools will tell you that you spend too much on subscriptions. Very few will tell you which one to cancel, which debt to pay first, or whether refinancing your car loan right now actually makes sense given your credit profile. That gap between insight and action is where a lot of people lose money quietly, every month, for years.

The category is enormous. Global fintech investment rebounded to $116 billion across nearly 5,000 deals in 2025, according to KPMG. Fortune Business Insights puts the broader fintech market at roughly $395 billion in 2025, with projections well past $1.7 trillion by the end of the decade. There is no shortage of capital or ambition here.

What there is a shortage of is products that close the loop. Mint told you where your money went. YNAB asks you to plan where it will go. Rocket Money will cancel your subscriptions if you ask it to. Credit Karma will surface a loan offer and call that a recommendation. None of these are bad tools. But they all stop short of what a financially literate friend would actually do, which is look at your full picture and say: here is the specific thing you should do next, and here is why.

AI is the obvious lever to pull here. Personalization at scale, pattern recognition across financial products, natural language interfaces that don’t require you to already understand what you’re looking at. The question is whether any given product is actually using that lever well, or just gluing a chatbot onto a spreadsheet and calling it intelligence. The same question applies to AI tools across categories, and the answer is usually somewhere uncomfortable in the middle.

SuperMoney has been in the financial services comparison space for a while. The new product is a bet that comparison is the beginning, not the end.

The Micro: Comparison Site Grows a Brain

SuperMoney’s original product was a financial services comparison platform. Think NerdWallet territory: shop for loans, compare credit cards, see your options side by side. According to Crunchbase, millions of people have used it for that. The company, founded and led by CEO Miron Lulic, has made the Inc. 5000 list five years running, according to a LinkedIn post from Lulic himself. That is a meaningful signal of sustained revenue, even if the underlying numbers aren’t public.

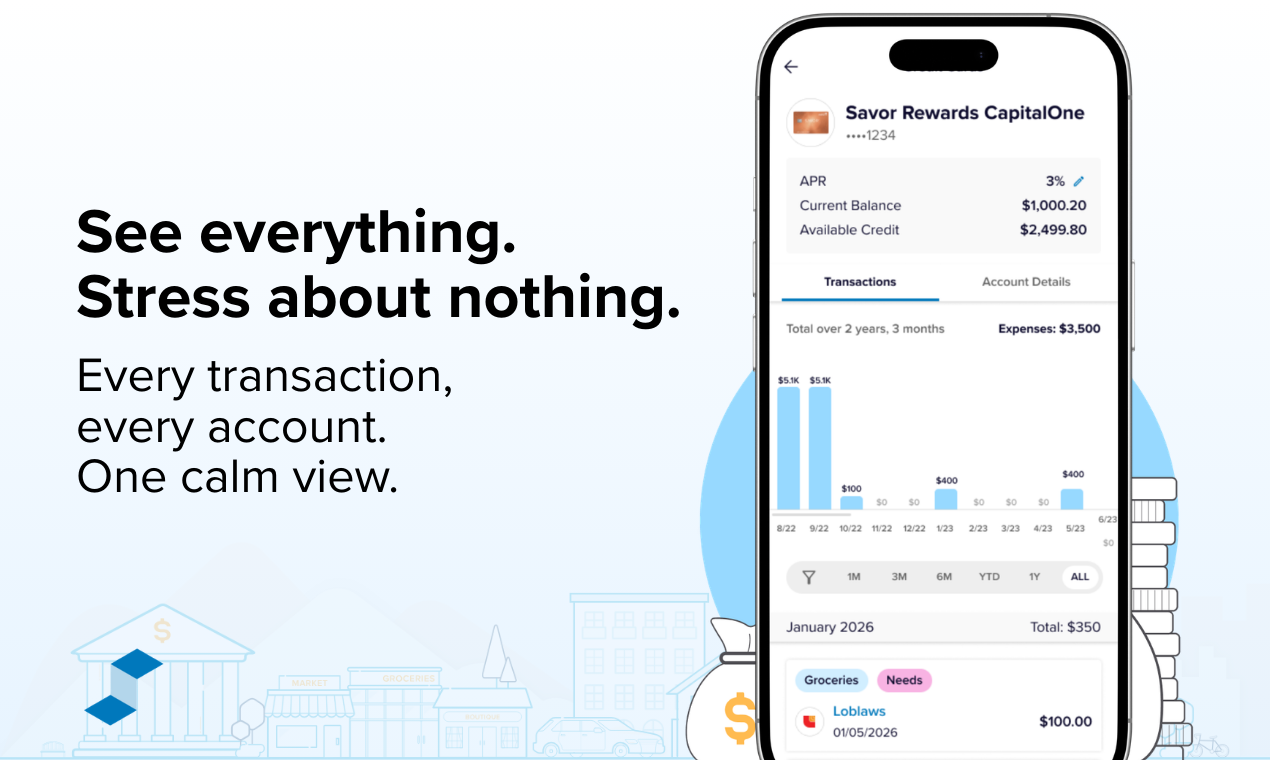

The new version goes further. The pitch is that SuperMoney now surfaces specific actions, not just information. Optimize your debt stack. Identify better financial products for your situation. Stay on a plan. The language the company uses is “you always know what to do next,” and that framing is doing a lot of work.

From what’s available publicly, the app connects to your financial accounts, analyzes your current debt, spending, and product mix, and then generates recommendations with context. It’s less “here are five balance transfer cards” and more “given your current APR and balance, here’s what moving this debt would save you over 18 months.”

The interesting product decision is that SuperMoney already has relationships with financial product providers. This isn’t a cold start on the data side. Whether those existing commercial relationships create any tension with genuinely neutral recommendations is a fair question, and one I’d want answered clearly before I handed over my bank login. Transparency about how AI-driven recommendations are generated is increasingly the thing users actually care about, even when they don’t know how to ask for it.

It got solid traction on launch day. 56 comments suggests real engagement, not just upvote farming.

The tagline is “your money stress, solved by AI.” That is a very large promise. Stress is not a feature.

The Verdict

I think the underlying insight here is correct. Comparison is a commodity. Action is the product people actually want. And SuperMoney has something most AI finance startups don’t, which is years of distribution, existing lender relationships, and a user base that already trusts it with financial decisions.

The risk is that the AI layer is thin. If the recommendations are just comparison results dressed up with a confidence interval and a conversational UI, sophisticated users will notice quickly and the trust that took years to build erodes fast. The 30-day question I’d ask is: are users completing the recommended actions, or reading them and closing the app?

At 60 days, I’d want to know whether the recommendation quality holds across different financial profiles. A tool that’s great at helping someone refinance a car loan and useless at helping someone with irregular income manage cash flow isn’t really solving money stress. It’s solving a specific, relatively easy problem.

At 90 days, the existential question: do the commercial relationships stay out of the recommendations, or do they quietly shape them? That answer will determine whether SuperMoney becomes genuinely useful or just a more expensive lead generation product in a better coat.

The foundation is real. Whether the new product earns the tagline is an open question, and I mean that as an honest assessment, not a dismissal.